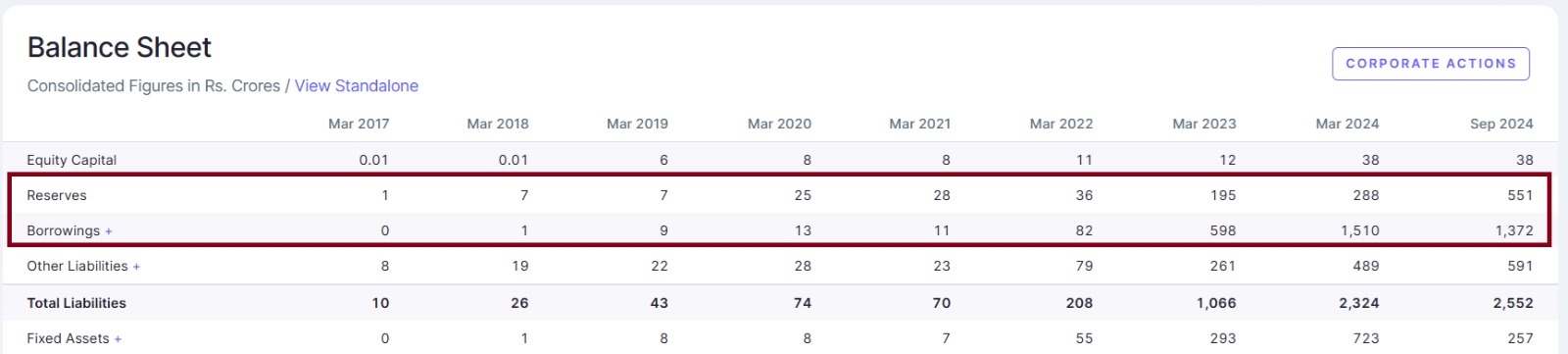

The biggest concern here is that the company’s market capitalization is INR 900 crore, while its debt has surged to INR 1372 crore. This means the company has borrowed more than its own capital, which is a serious red flag. If the company’s operations or cash flow do not remain strong, it might struggle to repay its debt.

However, the biggest red flag is that 81.7% of the company’s shares are pledged! 😨 This is a highly negative sign because it means that the promoters have used their holdings as collateral for loans. If the company’s financials weaken or the stock price drops, lenders may sell these pledged shares, further pressuring the stock.

Borrowings are Continuously Increasing! 📈

In 2017, the company had zero borrowings, but by 2024, it has surged to INR 1510 crore. This suggests that the company is operating with high leverage, which could be risky. Moreover, its reserves are not strong enough to handle a financial crisis or clear debts in the future.

Promoters Have a Strong Holding, But No Institutional Interest!

Promoters hold 62.66% of the shares as of Dec 2024, which is a positive sign, as it shows their continued involvement in the company.

However, there is zero FII or DII holding, meaning institutional investors are not interested in this stock, which is a negative signal.

A large portion of the stock is held by the public, and the stock float appears to be low.

Biggest Risk: Public Sentiment 😬

If the company fails to show revenue growth or does not meet public expectations, retail investors might start selling their shares in panic. This could create heavy selling pressure and further drag down the stock price.

Final Verdict: Gensol’s high debt and pledged shares are major red flags. Unless the company significantly improves its financial performance or attracts strong institutional investors, the stock will remain in a high-risk zone. Investors should carefully evaluate the risks before making any decisions!