ERIS Lifesciences Ltd: Growth or Red Flags? 🤔📈

A significant momentum is visible in an important pharmaceutical stock—ERIS Lifesciences Ltd! 🚀 Some aspects appear positive, indicating that the stock might perform well in the future, but at the same time, some red flags raise concerns. Let’s dive into an in-depth analysis! 👇

📊 Company Overview & Market Cap

ERIS Lifesciences Ltd is a pharmaceutical manufacturing & marketing company with a market capitalization of ₹18,460 crore.

🔹 Revenue Growth: In March 2013, sales were ₹393 crore, which grew to ₹2,009 crore in March 2024—a 5x increase! 🚀

🔹 Operating Margin: The company’s operating margin% is continuously improving, signaling strong profitability.

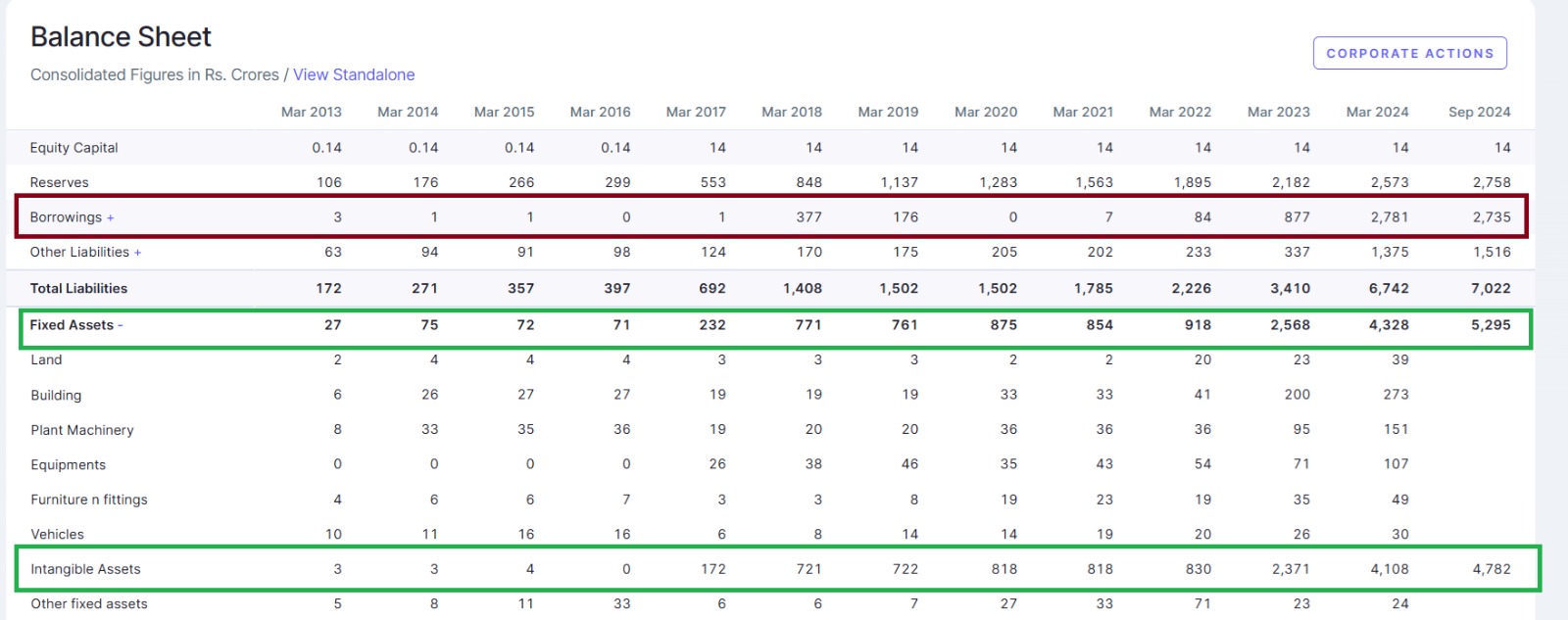

⚠️ Borrowing & Interest Expense – A Major Concern?

A red flag here is that the company’s interest expense has suddenly increased:

📌 March 2013: Interest ₹1 crore

📌 March 2024: Interest ₹210 crore ❗

➡️ Why? Because the company has taken aggressive borrowings, most of which have been invested in fixed assets.

📌 Fixed Asset Growth:

🔹 March 2013: ₹27 crore

🔹 September 2024: ₹5,295 crore 😳 (Massive jump!)

📌 Intangible Asset Investment:

The company has made major investments in acquisitions, including intangible assets. This could be positive for future growth, but it increases risk if the acquisitions fail to generate expected returns.

📉 Reserves vs Borrowing – A Risky Equation?

The company’s reserves have also consistently increased:

📌 March 2013: ₹106 crore

📌 September 2024: ₹2,758 crore

➡️ But there’s a problem! 🤔

The company’s reserves have grown at the same pace as its borrowings, meaning that if expected revenue is not generated from capex, there could be challenges in interest payments.

📌 What’s the risk?

If the company is forced to repay debt at once, its reserves may not be sufficient to cover it. This could put pressure on net profits.

📢 Management’s Plan on Debt Reduction

In the Q3 FY25 earnings call, the company stated that it plans to reduce its debt soon, with a major focus on debt repayment. This is a positive signal, but execution will be key.

📊 Shareholding Pattern – Mixed Signals!

1️⃣ Promoters Holding: 54.86% as of December 2024

➡️ However, a red flag! ❌

🔹 18.5% of the promoter’s holding is pledged – this indicates risk, as it means promoters have used their shares as collateral for loans.

2️⃣ Public Holding: 18.73%

➡️ Most of the public shareholders appear to be close associates of the promoters, raising concerns for retail investors. ⚠️

3️⃣ FII’s Holding: Continuously declining

📌 March 2022: 13.31%

📌 December 2024: 8.36% 😬

➡️ Foreign investors are losing confidence, which could be a negative signal.

4️⃣ DII’s Holding: Increasing steadily

📌 March 2024: 23.52%

📌 December 2024: 18.07%

➡️ Domestic Institutional Investors seem confident in the company’s prospects.

🚦 Final Verdict: Growth or Risk?

✅ Positives:

✔️ Strong revenue & operating margin growth

✔️ Capex-driven business expansion

✔️ Management focus on debt reduction

❌ Red Flags:

⚠️ Rising interest costs

⚠️ Imbalance between borrowings & reserves

⚠️ Promoter share pledging

⚠️ Declining FII holding

If the company successfully generates strong revenue from its capex and reduces debt, the stock could see long-term growth. However, if the debt burden continues, profitability may come under pressure.

🔍 Retail investors should stay cautious! 🧐 Future performance will depend on the company’s debt reduction strategy. 🚀